Brace yourselves everyone…I’m about to get REAL in today’s blog post…I’m not holding back, it’s my blog and I can say what I want, which is probably the last great thing remaining about this country since health care is going down the tubes. Anyway, this is my story on how Obamacare affects my family and I’m just being brutally honest with you all.

Today I got the dreaded insurance letter. I was hopeful it wouldn’t come; I figured our plan was already compliant given that we pay $468/month for health insurance and have a $5K deductible. Surely that’s profitable for the insurance co. and makes sense for both parties. My line of thinking was that our current plan is not cheap so it’s not going to change, right? Unfortunately, our plan is not compliant with the (un)affordable health care law. We can keep our plan until December 2014 with Humana, but then we have to get our butts in gear and have coverage that is in line with the law. I’m so glad the government knows exactly how to take care of my family and me and I’m glad to put our decisions into their hands.

In 2014, our plan will go up to $653/month. SUPER! I can’t wait!! My standard of living is about to explode with new health care benefits!!!!

As two self employed business owners, Rob and I have been paying for our own health insurance for six years now…and I believe we’ve always been responsible adults, picking a plan that has good coverage, even if it means a higher deductible b/c we want to keep our monthly cost low, albeit $468 is not that low, but it’s got really good coverage too (or so I thought). If we have something happen where we need to go to the hospital, we’ll pay our $5K and get on with our lives. Interestingly, our deductible goes down to $4K with the new plan, but it’s still right around $200 more a month equaling about $2400 more a year…I know I’m terrible at math, but I’m pretty sure this is less affordable than our current coverage. On the upside, if I decide to get a substance abuse problem, my care to get better is covered. Good to know…

Thanks a lot, Obama (and all who voted) for cramming this law down my throat, riffling through my wallet and taking some extra change, preeeesh!

If you haven’t received a cancellation letter or notice of an increase in your health insurance premium, don’t worry…I’m sure it’s headed to a mailbox near you. If you’re self employed it seems guaranteed you’re not keeping your policy. If you work for a company who provides insurance, chances are your employer may not be able to afford bringing your health care up to par. Can you guess what a business owner might do if they can’t afford to cover you? Maybe cut your hours so you’re not full time (which has already started happening), or eliminate your job all together, or opt for paying the fine in lieu of offering health care coverage, meaning your expenses just went up a whole heck of a lot and your income did not.

Or, maybe your employer will change from having employees to 1099 independent contractors. What does that mean? Well let me tell you since I’ve been a 1099 independent contractor for eight years as a Realtor. I don’t have any taxes taken out of my checks; I have to pay taxes quarterly…you feel a lot differently toward the government when you’re constantly writing them checks. And, 1099 folks don’t get unemployment, remember you’re not an employee; you’re an independent contractor. I wouldn’t be surprised if some businesses change to this model of “employment” in order to save money and continue profitability.

What the government doesn’t seem to understand, is that in order for there to be jobs, companies need to be profitable to hire employees, so if healthcare changes that, business owners will adapt…health care companies have adapted to the health care law by raising rates in order to do what the government now requires at a minimum.

My husband, who sells home, auto and commercial insurance put it to me this way:

Imagine the government telling everyone they need to own a car. Now, if you like your car, you can keep it (Thank GOD…b/c you know what, I actually love my car). The government can provide credits, if you qualify, for the car you’ll have to buy, but the fact of the matter is that everyone…EVERYONE has to own one now b/c it’s the law. But it’s a good thing really…you need to get around, and a car does just that. Now, the car has to be a Cadillac Escalade, it just has to be b/c that’s got the minimum standards the government requires. It’s got to have GPS b/c you need to know where you’re going and it has to have rims…b/c come on, who doesn’t love shiny, baller rims, right? And don’t forget the leather…leather is great b/c you can spill a drink and it doesn’t stain…we need to keep the resale value of these cars up, it’s good for the economy.

Oh Darn. You know what…there’s actually something I forgot to mention…that two-door coupe you have from 1999…weeeelllll, it doesn’t meet the minimum standards. I know it works for you and I said you could keep it, but really, you have to get rid of it. Sorry about that…but now you get to have a Cadillac Escalade!!

I digress…

Back to the cost of insurance…there are people (actuaries) whose only job it is, is to assess the risk of potential situations based on factual data. An actuary is defined as a person who computes insurance premium rates, dividends, risks, etc., based on statistical data. So when women are typically charged more for health insurance b/c…oh, I don’t know, they push human beings out of their body that makes sense to me. It also makes sense that a 16-year-old male driver has higher insurance rates, b/c they drive like they have nothing to lose.

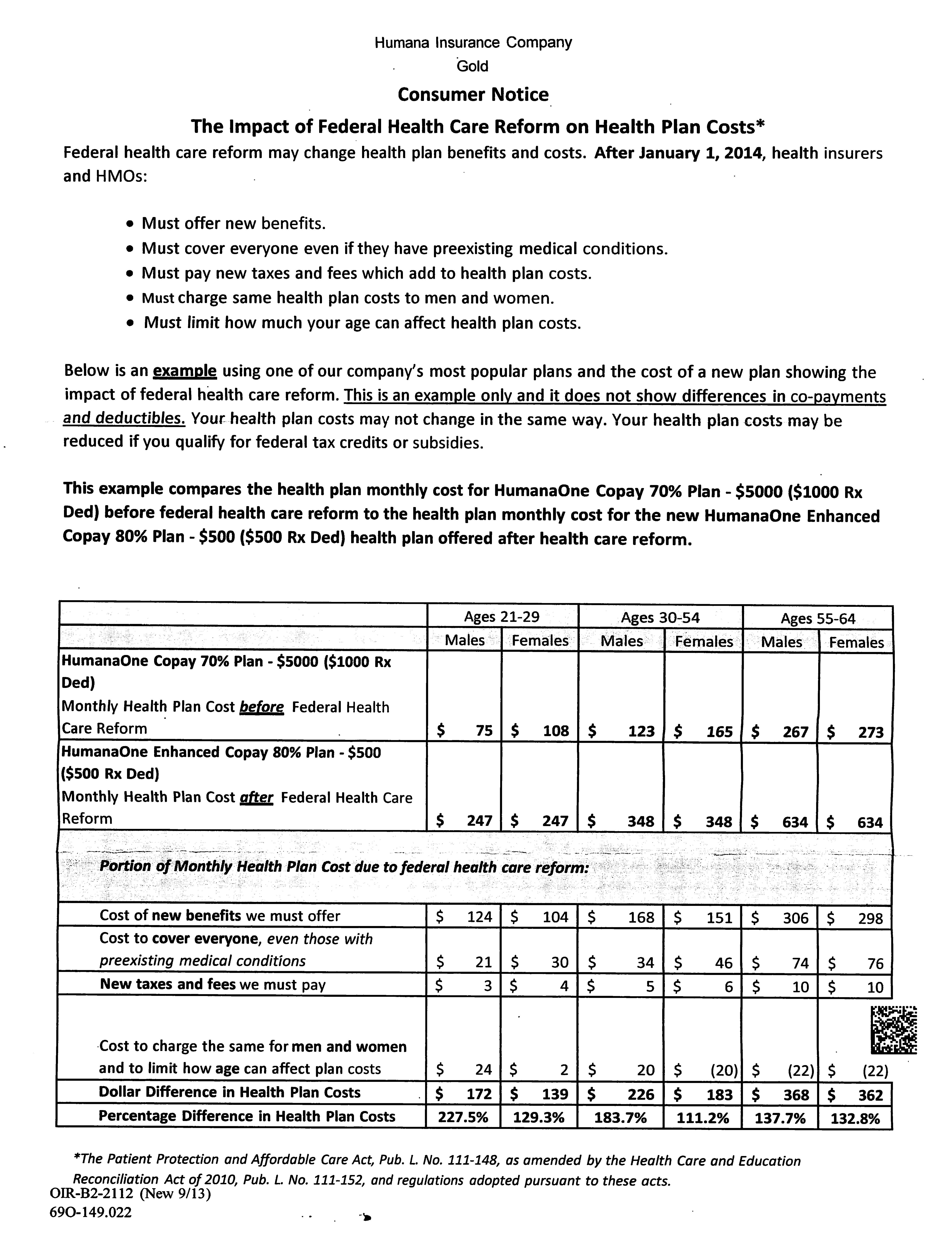

The most interesting part of the letter I received is the Consumer Notice that was included. I decided to share it with you here as I’m pretty sure it’s applicable to everyone.

How screwed are folks ages 55-64 who have been planning for retirement their entire lives? An increase from about $270/month to $634/month…hope you enjoy retirement, you’ve worked so hard…oh wait…maybe you will need to work a little longer to have the type of retirement you were hoping for. Thanks for your contribution to our socialistic health care…we appreciate YOU!

Sorry males ages 21-29, your health care costs just went up 227.5%. I know there’s all this statistical data from actuaries that says typically your health insurance risks are very small, but the good news is that you can stay on your parents plan until age 26. Although, I’m pretty sure someone is picking up the slack on that ridiculous difference. The government knows what’s best for you and your wallet, as well as your parents.

I could be totally off base in my assumptions, but I’m thinking those that voted for this were waaaaay off in what they thought this would be…remember, you had to pass the law to find out what’s in it.

What a terrific way to run a country! You know, let’s drop this massive bomb on the people and then see what their reaction is. I don’t like thinking things through…especially with my life and livelihood. Let’s just be reckless and stupid with everyone and deal with the consequences later.

Also, can someone tell me if anyone that works for the government knows of someone out there who can properly build a website that can handle the high volume that say Amazon, Facebook, Twitter, Pinterest and YouTube…do we know how to do that yet or is that beyond our capabilities?

Who else is loving this second term? I just can’t get enough…government shutdowns, an increase in my monthly expenses to meet new human requirements…it’s like rainbow sprinkles all over my living room.

Seriously, is this not the worst disaster ever? I think it’s kind of a BFD, bigger than Biden originally thought.

I told you I was getting REAL. You can disagree with me, but that’s my opinion and I’m sharing it. Who promises something to everyone in the country and blatantly breaks it? I like the Band-Aid fix of keeping my policy for a year, yeah…that’s not what you promised either. The entire premise of the law, what Obama said in order for Americans to trust him and in order for this to be voted law is proving to be a lie. And I believe a lot of presidents and politicians lie, I believe that everyone lies and breaks promises whether intentional or unintentional. But to watch this health care policy unfold into law is a total nightmare failure. People always rise to the level of their incompetence, and this my friends is one for the record books.

Obama: “If you like your health care, you can keep it…period.”

Oh wait…

A few final thoughts…

I think it’s good that insurance co’s. can’t prevent folks with pre-existing conditions from getting coverage, but those folks who are considered lower risk now have to contribute to those that are higher risk. And is healthcare really more affordable for people with pre-existing conditions? Or is it still out of reach? I truly don’t know. And why are we all required to carry minimum standards that increase our monthly expenditures? It’s crazy for the government to think there’s a one size fits all for health insurance…people are not one size fits all, but I do appreciate the effort to squeeze a square peg into a round hole.

Please feel free to share your healthcare story below.

November 25th, 2013 at 10:57 pm

Well said!

November 27th, 2013 at 1:09 am

Dan’s company got a letter from their insurance broker saying their premium is going up 40%. 40%!!!!!??? It already costs us $600/mo out of his paycheck because the company is too small for a group discount. Looks like we’ll be shopping around too.

November 27th, 2013 at 2:03 am

Rebekah, that is so ridiculous…this is happening to so many people, it’s just terrible.

December 5th, 2013 at 5:37 pm

Great article. Very well said! My husband and I also both self employed and we just got this letter last week.

December 5th, 2013 at 8:18 pm

WAAAAAHHHHHHH!!!!

December 5th, 2013 at 10:31 pm

Let me give it to you from the other side of the fence: My sister, age 61, a two time cancer survivor (thyroid when she was 42, and breast cancer 4 years ago) has been paying $1,000.00/month for the last 3 years, just for herself. She has a $10,500 deductible, no prescription coverage, and once she pays the deductible, gets the joy of paying 30% of all remaining bills.

Your daughter, if not for the ACA, would be considered as having a pre-existing condition and would be basically uninsurable. My grandson was $999,975.00 his first 9 months of life, and if not for the ACA would be uninsurable. My BFF, has been paying $1200/month with a $9,000 deductible just for herself for the last few years. She and her husband are both Realtors. He went on Medicare a couple of years ago, before that they were paying $24,000.00/year just in premiums!! And this kind of thing is nothing new….I was talking to my 85 year old mom, she was unable to get insurance when she was in her 50’s, due to a pre-existing condition (hot flashes, for crying out loud!). So, $468 is cheap, and the $600 really isn’t too bad. Just wait until you hit the magic number of 40, then 50….

December 9th, 2013 at 4:58 pm

Thanks for sharing, Jill…and I think that’s ridiculous. Those premiums and costs are out of control. But like I said in the post, is it fair to make folks who are lower risk pay for those who are higher risk? Health care needed some change, but I don’t know that this was the answer. Out of curiosity, what do the premiums look like for your sister and grandson now?

January 21st, 2014 at 9:29 pm

Sorry, AM…just saw this. My sister is paying about $350.00 per month for herself for a silver plan. Her deductible is $3000, but that’s what she wants to live with and considering what she was paying, to her that is cheap. Plus, her co-pay is now 20% instead of 30% and she has prescription coverage, which she didn’t have before. She does live in Washington state. My bff decided just to suck it up and not sign up since she will be 65 in March and will be going on Medicare. My grandson’s mom ended up putting all three of her kids on Medicaid and said the oldest one with the issues is getting better care now than when she was on insurance with her employer.

John and I went for a gold plan. We went with a BC/BS ppo plan. It is costing us $602/month (after subsidy), we pay out of pocket the first $1300 each, (no co-pays, however) with a $10% of any charges after that up to a total max out of pocket of $2600/year (each) and that includes any prescription costs. And for some reason when we move later this year, the $602 will go down to $358/month for the both of us. Under John’s former employer we were paying $375/month for each of us, with a $40 copay for a family practitioner, $50 co-pay for a specialist, $200 co-pay for emergency room, $75 copay for any Centra-care type places,and whole host of other co-pays…e.g $40 for each physical therapy visit, a separate $100 deductible (each) for prescriptions, and a $2500.00 out of pocket max per year.

The object of insurance is to spread the risk around, which is why those people who are low-risk are seeing their ins go up. Although my son (36, works for Enterprise RAC) said his went down this year.

January 22nd, 2014 at 8:12 pm

We got our letter in November that our plan will expire in April. I honestly haven’t bothered looking up the new rates yet, been too busy with the holidays and annoyed by the whole thing. We could barely afford our current coverage that doesn’t even include our youngest yet, so I’m not too positive this is going to work out better for us. Sigh.